Introduction: PAS-6 Applicability

Understanding PAS-6 applicability is crucial for companies dealing with share capital compliance in India. However, confusion still exists among professionals and business owners regarding when PAS-6 becomes mandatory.

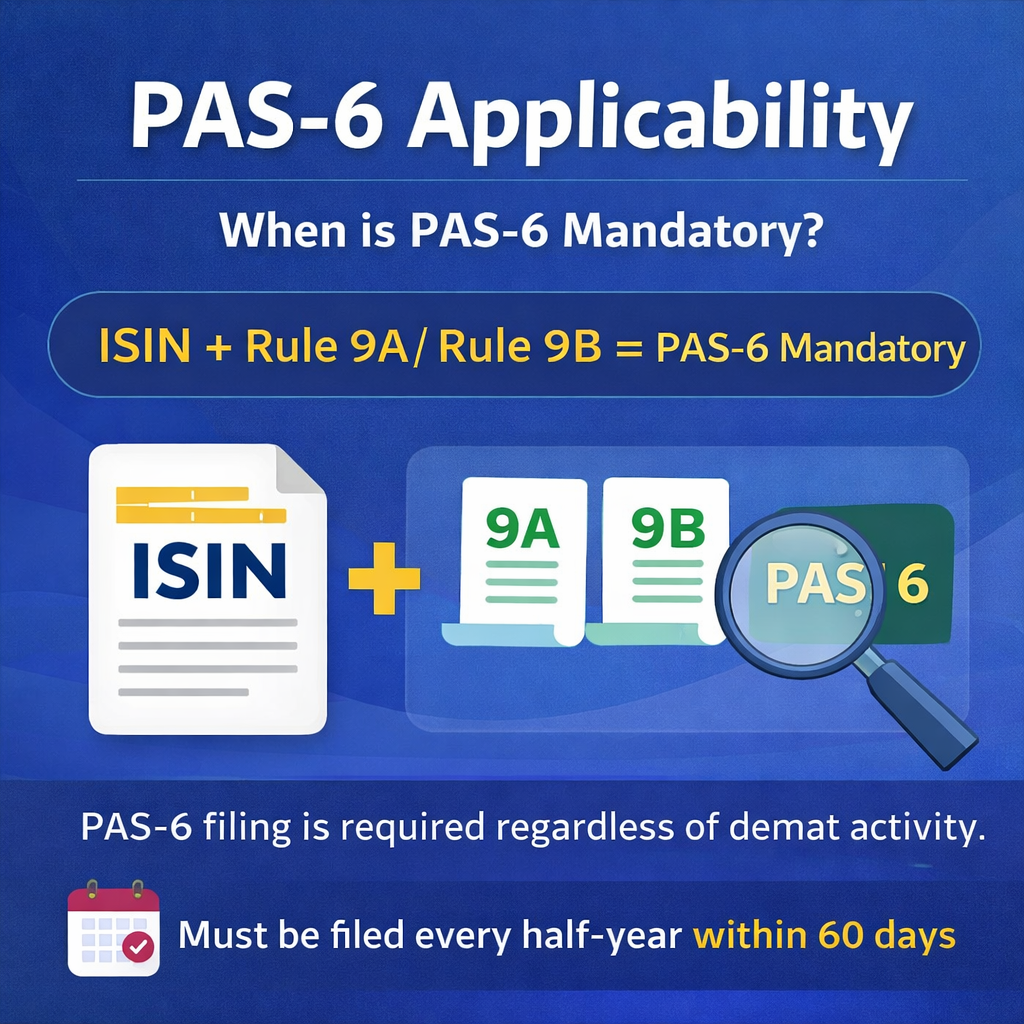

Many assume that PAS-6 is required only when shares are dematerialized. However, this is not correct.

The applicability depends on a simple compliance logic:

ISIN + Rule 9A / Rule 9B Applicability = PAS-6 Mandatory

Therefore, even if no shares are dematerialized, filing may still be required. This guide explains everything with practical, scenario-based clarity.

What is PAS-6?

PAS-6 is a reconciliation of the share capital audit report. It ensures consistency between:

- Physical share capital

- Dematerialized shares

- Total issued capital

- Depository records

In addition, it helps regulators monitor shareholding transparency and prevent discrepancies.

Basic Rule of PAS-6 Applicability

PAS-6 becomes mandatory when:

- The company has obtained an ISIN, and

- The company falls under Rule 9A applicability or Rule 9B applicability to a private company

Therefore, both conditions must be satisfied.

Simple Compliance Formula

- ISIN obtained

- Covered under Rule 9A or Rule 9B

PAS-6 filing is compulsory

Moreover, this rule applies regardless of demat activity.

PAS-6 Applicability for an Unlisted Public Company

Under Rule 9A applicability, every unlisted public company must:

- Facilitate dematerialisation of shares

- Obtain ISIN

- Maintain compliance with depositories

As a result, once an ISIN is obtained:

PAS-6 filing becomes mandatory

Key Insight:

Even if shareholders have not converted shares into demat form, PAS-6 must still be filed.

PAS-6 Applicability for a Private Company

The rules changed with the introduction of Rule 9B applicability to a private company.

Now:

- Private companies (other than small companies) must comply with dematerialization requirements.

- ISIN is required

Therefore, PAS-6 is mandatory after obtaining ISIN

PAS-6 Applicability to a Small Company

This is where most confusion arises.

Case 1: Small Company WITH ISIN

- ISIN may be obtained voluntarily.

- However, Rule 9A/9B does not apply.

PAS-6 is NOT mandatory

Case 2: Small Company WITHOUT ISIN

PAS-6 is not applicable

Hence, small companies are generally outside PAS-6 compliance unless regulations change.

PAS-6 Mandatory or Not?

|

Scenario |

PAS-6 Required? |

|

Unlisted Public Company with ISIN |

Yes |

|

Private Company (not small) with ISIN |

Yes |

|

Private Company (not small) without ISIN |

No (until ISIN obtained) |

|

Small Company with ISIN |

No |

|

Small Company without ISIN |

Not Applicable |

PAS-6 Due Date

Understanding the PAS-6 due date is essential to avoid penalties.

PAS-6 must be filed half-yearly within 60 days:

- April – September – Due by 29th November

- October – March – Due by 30th May

Timely filing ensures compliance and avoids legal complications.

PAS-6 Filing Process

The PAS-6 filing process involves the following steps:

Step 1: Obtain ISIN

Coordinate with a depository participant.

Step 2: Collect Share Capital Data

Gather details of:

- Physical shares

- Demat shares

- Issued capital

Step 3: Reconciliation

Match company records with depository data.

Step 4: Certification

The report must be certified by:

- Practicing Company Secretary, or

- Chartered Accountant

Step 5: File with MCA

Submit PAS-6 through the MCA portal.

Proper documentation is critical for smooth filing.

PAS-6 Penalty for Non-Filing

Non-compliance can lead to serious consequences.

Penalties include:

- Monetary fines on the company

- Penalties on officers in default

- Regulatory scrutiny

Therefore, timely filing is not optional—it is essential.

ISIN Requirement for PAS-6

The ISIN requirement for PAS-6 is the most critical trigger point.

Without ISIN:

- PAS-6 is not applicable

With ISIN + Rule 9A/9B:

- PAS-6 becomes mandatory

Hence, obtaining ISIN automatically increases compliance responsibility.

Practical Example for Better Understanding

Example 1:

A private company (not small) obtains an ISIN.

- Covered under Rule 9B

- PAS-6 required

Example 2:

An unlisted public company has an ISIN.

- Covered under Rule 9A

- PAS-6 mandatory

Example 3:

A small company voluntarily takes an ISIN.

- Rule 9A/9B not applicable

- PAS-6 not required

How R A Daga and Co. Can Help

As a professional company secretary firm, we assist with the following:

- PAS-6 applicability analysis

- ISIN advisory and coordination

- End-to-end filing support

- Compliance tracking and reminders

- Certification and documentation

Our goal is to simplify compliance and eliminate risks.

Conclusion

- PAS-6 applicability depends on ISIN + Rule 9A/9B

- It is not dependent on dematerialisation

- Private and unlisted public companies must comply once ISIN is obtained.

- Small companies are generally exempt.

Therefore, understanding this framework ensures smooth compliance.

Call us now: +91 80870 64602 or visit radaga.in/contact-us for quick assistance.